The best way to stop the massive under-taxation of Australian LNG would be to fix the petroleum resource rent tax, but a quick second best would be a tax on export revenue.

The Australian gas industry is paying ridiculously low rates of tax. The resources that they are mining belong to all of us, not just them, but many Australian offshore gas fields pay no royalties, with approximately 56 per cent of exported gas being royalty-free.

Instead, offshore gas is meant to pay the petroleum resource rent tax, but it is poorly designed. Indeed, as recently as 2023, the Treasury wrote that so far no LNG project had ever paid any PRRT; not even in 2022 when gas prices shot up by four or five times, in response to the cutting-off of Russian gas supplies.

According to the investment advisory firm, Stocks Down Under: “Australia captures less than 30 per cent of profits from its fossil fuel companies, compared to 75-90 per cent in most comparable resource-exporting nations”. Australia Institute research shows that between 2015-16 and 2023-24, the revenue from Australian gas exports has increased more than five times, but Australian government tax revenue from gas exports hardly increased at all.

Furthermore, because of the impact of the Iran War on gas supplies and prices, the profits from gas sales have risen substantially, so we are missing out on even more tax revenue.

In short, the Australian government, which is experiencing considerable budget pressures, should be considering how they might raise additional revenue by increasing the taxation of excessive mining profits or rents.

But instead, the opposition leader, Angus Taylor, claimed at a Parliamentary Enquiry that “a 25 per cent tax would close down the gas industry and that is the intent of that tax”.

Now even more importantly, the ABC reports that the Prime Minister, Anthony Albanese, is poised to kill off any move to increase taxes on gas giants in the forthcoming budget. Although the Prime Minister’s own department requested modelling of options to raise more revenue from the industry, the Prime Minister now seems to think, after visiting our energy trading partners and listening to the gas producers, that this is not the time to be hiking taxes on the LNG that Australia is exporting.

Both the PM and Taylor are wrong. Taxing the super profits or rents being generated by the gas industry will not harm either gas production or the supply of gas exports to our trading partners.

Why increased taxation of gas can be production and price neutral

Our starting point must be to recognise that resource markets are very different from other markets.

In the conventional competitive market, the cost of production is typically much the same for all producers, and no producer gains an excessive profit or rent. But the reason why resource markets are very different is because some resources are very easy to mine, while others cost a lot to mine.

For a given level of demand, the resource price will typically be determined by the cost of production in the marginal resource mine which must get a price that provides an adequate return on its investment. But that price will then provide a higher return, or rent, than all the other mines need to justify their investment.

Furthermore, when war causes supply shortages that cannot be quickly remedied, then prices rise so high that even the marginal resource mine will be generating an excessive profit.

Finally, these resources do not really belong to the miner, but to us – the community – and we should receive some payment for transferring ownership of these resources to the miner so that it can exploit and sell them at an excessive profit. But as already noted, typically offshore gas does not even pay royalties.

So how should excess gas profits be taxed?

The petroleum resource rent tax (PRRT) was intended to be the optimum way of taxing resource rents. However, in practice it has not worked and, as noted above, at least until very recently it did not raise any money.

Ideally the PRRT would be amended so that it met its intent of taxing super profits or rents more completely. In addition, the tax rate could be increased from 40 per cent as this is much lower than in say, Norway where oil companies’ taxes take roughly 78 per cent of their profits.

But any such reforms could take time to develop successfully. Instead, a quick response to the very high profits now being generated by the Iran War would be to adopt the ACTU proposal for a 25 per cent flat tax on the value of gas exports.

Furthermore, contrary to the self-interested claims by the gas industry, this tax will not damage either production or exports at all. The producers will still be left with a much more than adequate return on their production and export sales so why should they cease producing and exporting?

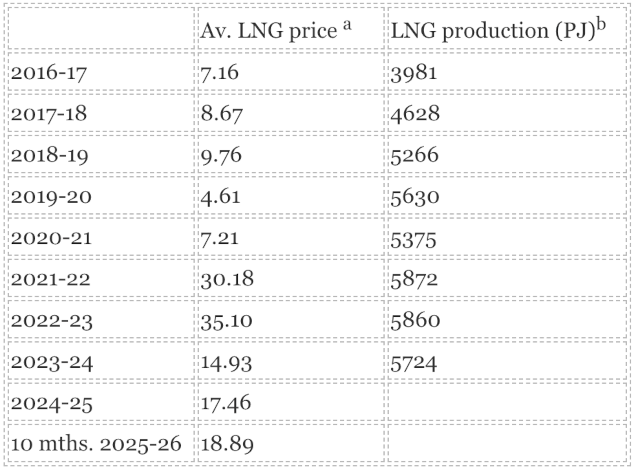

In fact, experience is that over time LNG prices have fluctuated extremely but that has not made any difference to production (see Table 1). Indeed, in 2019-20, the LNG price halved compared to the previous year, but production increased. Similarly, the volume of export sales has been equally stable at around 83 per cent of production since production reached its present level in 2019-20.

However, the value of LNG exports does fluctuate enormously. Although 75-80 per cent of LNG export sales are governed by long-term contracts, these contracts only cover the volume to be supplied and the LNG contract prices are linked to Asian LNG spot market prices and crude oil prices.

The latest price data show that in April the price for a gigajoule of gas was $18.45. This most recent price is more than four times the price of $4.61 back in 2019-20. So if it was economic to produce gas back then at a quarter of today’s prices, it would still be very advantageous to produce and export gas today, even if 25 per cent of the export takings are lost to taxation.

Table 1 LNG prices and production

Indeed, arguably in present circumstances this export tax should be higher, and Albanese should stop being so timid and so readily influenced by self-interested businessmen who are contradicted by the evidence.

As the former Treasury Secretary and Australia’s leading tax expert, Ken Henry, testified to a Parliamentary Committee: “Just do it, in the national interest, just do it, and stop the crap that the Australian public have put up with for decades now in respect of taxation of Australia’s finite resources.”

Michael Keating is a former Secretary of the Departments of Prime Minister and Cabinet, Finance and Employment, and Industrial Relations. He is presently a visiting fellow at the Australian National University.